Table of Contents

When someone asks me about the standard of Deferred payment, I often describe it in a simple way. In the complex architecture of modern macroeconomics assignment help, money is often described by its most visible roles: the bills in your wallet used for coffee (medium of exchange) or the balance in your savings account (store of value). However, there is a “silent” function that underpins the entirety of the global credit market, the US housing industry, and international trade. This is the standard of deferred payment.

To make you better understand, I am sharing a standard definition of deferred payment. This helps to gain clarity on your overall concepts.

A standard of deferred payment is a function of money that allows it to serve as a measure for valuing and settling future debts. In the US, the dollar acts as this standard, ensuring that a $1,000 debt today is measured as $1,000 when paid back years later.

As we look toward 2026, with the potential introduction of Central Bank Digital Currencies (CBDCs) and shifting inflationary pressures, understanding what is standard of deferred payment in economics has never been more critical for consumers, investors, and students alike.

Understanding how money functions over time is vital for global trade. Access international economics assignment services to clarify these advanced monetary concepts.

Meaning of Standard of Deferred Payment

To provide a standard of deferred payment definition, we must look at how obligations are settled over time. A standard of deferred payment is a function of money that allows it to serve as a widely accepted measure for valuing and discharging future debts, and focuses on the debt settlement agreement. When you take out a loan today to be paid back in five years, the “standard” used to measure that future debt is money.

In a technical sense, the standard of deferred payment definition that economics experts use refers to the baseline used to determine the value of a debt. Without this function, credit transactions would be nearly impossible. If you borrowed three cows today, would you owe three cows in ten years? What if the cows are older or of a different breed? Money solves this by acting as the means of deferred payment, ensuring that the meaning of deferred payment is consistent across time and space.

When we ask what the meaning of the standard of deferred payment is, we are essentially asking how a society agrees to value its future. It is the yardstick for long-term obligations. Therefore, a standard of deferred payment meaning is intrinsically linked to the stability of the currency itself. If the value of money fluctuates wildly, it fails as a reliable standard.

While money defines the value of future payments, a definition of trademark identifies the unique symbols, logos, or words that distinguish a brand’s goods or services. Legally, it grants exclusive rights to the owner, preventing others from using confusingly similar marks and ensuring brand identity remains protected in the marketplace.

When I look at how modern economies actually function, the Standard of Deferred Payment isn’t just a textbook definition; it is the invisible glue of our finance assignment help lives. Modern economies do not just run on cash; they run on promises. Most people know money is a “Medium of Exchange” for buying lunch or clothes. But its most powerful job is being a Standard of Deferred Payment.

In my view, this function is what truly enables the massive scale of the American economy. Without a stable standard to measure future value, the credit markets we rely on—mortgages, student loans, and corporate bonds—would essentially freeze.

Think about these common tools:

You can think of this function as a “time machine” for value. It lets you enjoy the utility of a car or a house right now. In return, you sign a binding deal to pay back a specific amount of value later.

By acting as a reliable yardstick for future debt, money ensures that a promise made today still carries the same weight years down the road. Without it, our modern world of credit and big dreams simply wouldn’t work.

To understand how this works in practice, think of it as the point where different economic roles collide:

| Function | How it supports Deferred Payment |

|---|---|

| Unit of Account | Provides the specific “yardstick” used to measure the debt, ensuring both parties agree on the value owed. |

| Store of Value | Gives the creditor confidence that the money will still hold purchasing power when the debt is paid in the future. |

| Legal Tender Laws | Mandates the acceptance of the currency for all debts, public and private, removing settlement risk. |

The fourth function of money, a standard of deferred payment, is often considered an extension of the unit of account and store of value. However, it deserves its own category because it specifically addresses the dimension of time. Money serves as a standard of deferred payment when it is used to state the amount of a debt to be paid at a future date.

In the US market, the US Dollar is the supreme standard for deferred payment. Under federal law, the dollar is “legal tender for all debts, public and private.” This means that if you have a deferred amount, meaning a balance owed to a creditor, the creditor is legally obligated to accept U.S. dollars to settle that debt. This legal backing is why money as a standard of deferred payment is so effective in the American economy.

Ultimately, I believe this function is what transforms money from a simple tool for trade into a sophisticated engine for economic growth and long-term planning. Money serves as a vital tool for settling long-term debts globally. This function directly keeps banking systems and national credit stable over time. To understand how these currency systems operate, checking professional macroeconomics assignment help websites gives students clear answers.

You might wonder, how does money act as a standard of deferred payment in daily life? The process relies on the concept of “Legal Tender” and the stability of the standard of deferred payment function of money.

In simple terms, it is a rule that allows money to be used to settle debts in the future. When you sign a contract, you aren’t promising to pay back “three cows” or “ten bags of grain,” because the deferred payment plan definition specifies the principal amount in dollars. Instead, you promise to pay back a specific amount of Legal Tender (dollars).

While I explain the standard of deferred payment to a student, I suggest to explore economics dissertation topics to make a high-level research topic on the impact of deferred payments. I believe it helps to give the most suitable options to boost your scores. You might say: “It is the promise that the ‘units’ you borrow today are the same ‘units’ you pay back later, even if their purchasing power has slightly shifted.” This is why money standard of deferred payment is the bedrock of the banking system.

To truly grasp the standard of deferred payment meaning, it is helpful to look at standard of deferred payment examples in the current US economy. Here, you need to check out our business environment assignment help where experts are ready to share real-life examples and its application of deferred payment in business.

This is the most common example of the standard of deferred payment. When a homebuyer signs a 30-year mortgage, they are agreeing to a deferred payment plan meaning they will pay back a fixed or variable amount of dollars over three decades. The dollar acts as the standard that makes this long-term credit possible.

In a deferred payment in a sentence: “The graduate began her deferred payment plan six months after commencement, utilizing the US Dollar as the standard of deferred payments to settle her tuition debt.”

Using our Business Research papers, you definetely get an idea of BNPL. Modern fintech apps represent a contemporary standard of deferred payment example. When you purchase a $400 item and split it into four payments of $100, you are engaging in a credit transaction where the dollar is the standard deferred payment measure.

Large companies issue debt to be paid back in 10 or 20 years. Investors buy these bonds because they trust the money standard of deferred payment definition will remain stable enough to return their value with interest.

In my experience, a deferred cash payment is essentially a “buy now, pay later” arrangement between companies. If I’m a business owner buying new machinery, I might receive the equipment today but agree to pay the vendor in six months.

Deferred Cash Payment Meaning

This refers specifically to obligations that must be settled in physical or electronic currency at a later date, as opposed to “in-kind” payments (like trading stock).

Deferred compensation is income you earn now but receive later. This is often done to get tax perks. You might see this in big pay packages for leaders or in a deferred payment plan meaning for a new refrigerator. It also shows up in a multi-million dollar “deferred pay” athlete contract.

The basic idea is always the same. The standard of deferred payment function of money economics lets people agree on a value today. This allows them to finish a deal at a later date.

The primary threat to any standard for deferred payments is price instability. To understand what the standard of deferred payment means in a volatile market, we must look at how inflation and deflation affect debtors and creditors.

| Economic Condition | Effect on Standard of Deferred Payments | Who Wins? |

|---|---|---|

| Inflation | The real value of the money paid back is less than the value borrowed. | Debtors (They pay back “cheaper” dollars). |

| Deflation | The real value of the money paid back is more than the value borrowed. | Creditors (They receive “stronger” dollars). |

| Hyperinflation | The standard deferred payment meaning collapses; money is no longer accepted for future debt. | Barter System (Money fails its function). |

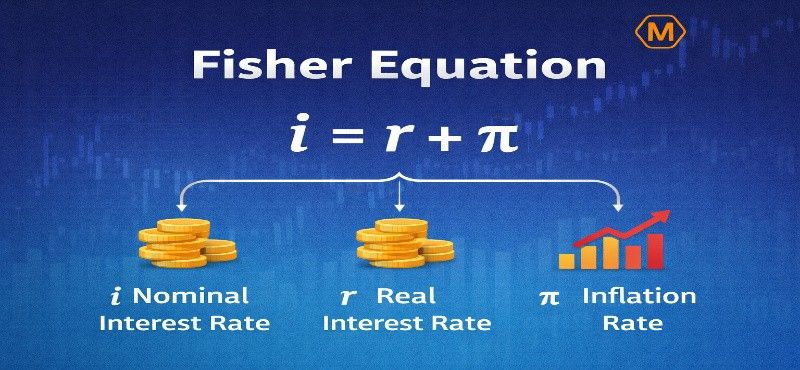

The Fisher Equation (r ≈ i – π) is the mathematical backbone of this analysis. It shows that the “Real Interest Rate” (r) is the “Nominal Interest Rate” (i) minus the “Inflation Rate” (π). If inflation is higher than expected, the standard of deferred payment effectively transfers wealth from the lender to the borrower.

As per my analysis, managing deferred payment topics can be a significant hurdle for students in the US, as these concepts sit at the intersection of complex financial regulations and university-specific policies. In that case, take guidance from our essay writing guide topics to make it easy to understand deferred payment topics. On top of classes, many students worry about how to pay for their education. Deferred payment plans allow students to attend school now and pay the bill later. While this helps at first, it creates many “pain points” or big problems for students.

The biggest problem is that the rules are confusing. Students must read long contracts with legal words. Many do not understand exactly when they need to start paying or how the “fine print” works. Without clear information, students often feel lost or tricked.

Many students think “deferred” means the cost stays the same. However, in many plans, interest keeps growing while the student is in class. This is called “accrued interest.” By the time a student graduates, the amount they owe may be much higher than the original price. This feels like a trap that makes the debt much harder to pay off.

The process to sign up for these plans is often very hard. Students are already busy with exams and homework. Filling out long forms for banks or the school takes a lot of time. If a student makes one small mistake or misses a deadline, they might lose their chance to delay the payment.

Knowing that a huge bill is waiting after graduation causes a lot of anxiety. This stress can make it hard to focus on studies. Some students worry so much about their future debt that their mental health and grades suffer.

Finally, it is often hard to get help. Schools and loan companies do not always give clear answers. Students often feel like they are solving a difficult puzzle all by themselves.

To solve these problems, colleges need to make the process simpler. Better education about money would help students feel more in control of their future.

These issues are strongly dealt with by our experts at MyAssignmentHelp, and we help in the following ways:

Assignments are handled by professionals of Accounting Assignment help with backgrounds in Finance, Law, and SEO-driven Content Strategy. This ensures that the content is not only factually correct but also structured using frameworks like the PEEL method (Point, Evidence, Explanation, Link) to ensure logical flow.

Experts tailor assignments to the specific regional requirements of the US education system, including:

Instead of just providing definitions, experts often include:

To better understand, check out our amortization schedule here:

An amortization schedule is a table that shows every payment on a loan. It breaks down how much of your money goes toward the original loan (principal) and how much goes toward the cost of borrowing (interest).

When a student loan has deferred interest, the borrower does not have to make payments while they are in school. However, interest still builds up. If this interest is “unsubsidized,” it is added to the total loan balance when repayment begins. This process is called capitalization.

In this example, we look at a $10,000 loan with a 6% annual interest rate. During four years of college, the borrower makes zero payments.

| Time Period | Action | Interest Added | New Total Balance |

|---|---|---|---|

| Year 0 | Loan Taken Out | $0 | $10,000 |

| Year 1 | In School | $600 | $10,600 |

| Year 2 | In School | $600 | $11,200 |

| Year 3 | In School | $600 | $11,800 |

| Year 4 | Graduation | $600 | $12,400 |

Once the “grace period” ends, the new balance of $12,400 is amortized. If the borrower chooses a 10-year (120 months) plan at 6%, the monthly payment is roughly $137.66.

Sample Amortization Table (First 6 Months)

| Month | Monthly Payment | Interest Portion | Principal Portion | Remaining Balance |

|---|---|---|---|---|

| 1 | $137.66 | $62.00 | $75.66 | $12,324.34 |

| 2 | $137.66 | $61.62 | $76.04 | $12,248.30 |

| 3 | $137.66 | $61.24 | $76.42 | $12,171.88 |

| 4 | $137.66 | $60.86 | $76.80 | $12,095.08 |

| 5 | $137.66 | $60.48 | $77.18 | $12,017.90 |

| 6 | $137.66 | $60.09 | $77.57 | $11,940.33 |

Visualizing the “hidden” cost of deferment is a powerful way to engage readers. It highlights why paying even $25 a month during school can save thousands in the long run. By showing the math clearly, you provide immediate value that helps students make better financial choices.

Every solution is passed through a multi-tier quality check:

So, whenever you get stuck on these critical topics, you are always welcome at MyAssignmentHelp expert services.

The evolution of money into a programmable asset via a Central Bank Digital Currency (CBDC) represents the most significant shift in the standard of deferred payment since the transition away from the gold standard. Historically, this function of money has been plagued by the “inflation risk” inherent in long-term contracts; if the value of the currency fluctuates significantly, either the debtor or the creditor unfairly loses purchasing power by the time the debt matures.

If the US transitions toward a more digitized standard, what is standard deferred payment will evolve. Programmable money could allow for “Smart Contracts” where deferred payments meaning becomes automated. For example, a deferred payment plan could be coded to automatically adjust based on real-time inflation data, ensuring that the money as a standard of deferred payment remains perfectly “fair” to both the creditor and the debtor.

Even with new tech, the core meaning of a standard of deferred payment stays the same. It is a legal contract. It lets us build the future today by promising value for tomorrow.

These new contracts offer several benefits:

While we are moving from paper to code, the goal is the same. Money remains a stable bridge of trust between what we use now and what we produce later.

Understanding what is the meaning of standard of deferred payment is essential for navigating the modern financial world. From the deferred payment examples of everyday credit cards to the massive scales of national debt, this function of money is what enables economic growth and personal financial planning.

My opinion helps to look toward the fiscal landscape of 2026; maintaining a stable standard of deferred payment is the top priority for the Federal Reserve. Whether through traditional fiat or a new digital dollar, the ability to define, measure, and settle future obligations is the “invisible hand” that keeps the wheels of commerce turning.

For anyone looking to define deferred payment or implement a deferred payment plan, remember that the stability of the currency is just as important as the terms of the contract itself. In the world of economics, money isn’t just about what you can buy today—it’s about the integrity of what you’ve promised for tomorrow.

It is the function of money that allows people to borrow and lend. It means that money is the official measure used to pay back a debt at a future date.

In the U.S. and many other countries, Bitcoin is not the main way people handle debt. Its price moves up and down very fast. If you borrowed one Bitcoin today, you might owe much more or much less in a year than you expected. This makes it hard to plan for the future.

Also, Bitcoin is not “legal tender.” This means the law does not force businesses or banks to accept it to pay off a debt. Most people still prefer to use dollars or other stable money because the value stays more predictable over time.

Beyond theoretical definitions, our professionals utilize practical financial modeling to clarify difficult concepts. This includes creating amortization schedules to demonstrate how deferred payments impact loan costs over 10 to 20 years, as well as providing comparative analyses between standard, deferred, and income-driven repayment (IDR) plans.

Yes. We understand that many students struggle with the complexity of accrued interest and the mathematical differences between subsidized and unsubsidized deferment. Our experts, who have backgrounds in Finance and Law, provide clear step-by-step breakdowns of how interest capitalizes during periods of non-payment.

Legal topics like the Master Promissory Note or the Higher Education Act are often hard to understand. They use many difficult words. Our experts are very good at explaining these rules clearly. We turn complex ideas into easy-to-read school papers. To do this, we use the PEEL method.

Each paragraph we write follows these four steps:

Using this plan helps keep your work organized and simple to follow.

If a currency experiences hyperinflation, people lose faith in its future value. They stop lending money, and the credit market collapses. People may return to a barter system or use a foreign currency (like the US Dollar in unstable regions) as their standard for deferred payment.

“Store of Value” means you can hold money and it will keep its value for you to spend later. “Standard of Deferred Payment” means that the money is used as the benchmark for a debt agreement between two different parties over time.

Our experts make sure your economics work fits perfectly in the American school system. We use US GAAP rules for all money-related math to keep things accurate. We also stay up to date with the latest Federal Student Aid rules.

Your paper will follow your school’s exact grading rubric. We can format your work in any style you need, including:

We have a strict multi-step check to make sure your work is top-notch. To prove your paper is unique, we give you a report showing it is 100% original. Every assignment is written by a real person—never by a bot.

If you have questions about a hard math formula or a new law, our team is here 24/7 to help. We are always ready to explain the details or make quick changes whenever you need them.

When money fails as a standard of deferred payment, the credit market collapses. Hyperinflation or instability makes future debt settlement unpredictable, forcing lenders to stop issuing loans. This destroys long-term investment, halts economic growth, and often pushes society back toward bartering or using stable foreign currencies to settle financial obligations.

In the evolving financial landscape of 2026, these roles are becoming even more critical. With the rise of Central Bank Digital Currencies (CBDCs), the standard of deferred payment is being digitized, potentially offering more transparency and stability for long-term credit contracts and future debt settlements on a global scale.

The US dollar is an ideal standard for deferred payment due to its relative price stability and global liquidity. Low inflation ensures that the value of a debt remains predictable over time. Additionally, its status as the world’s primary reserve currency provides a reliable, universally accepted benchmark for long-term contracts.

Hi, I am Mark, a Literature writer by profession. Fueled by a lifelong passion for Literature, story, and creative expression, I went on to get a PhD in creative writing. Over all these years, my passion has helped me manage a publication of my write ups in prominent websites and e-magazines. I have also been working part-time as a writing expert for myassignmenthelp.com for 5+ years now. It’s fun to guide students on academic write ups and bag those top grades like a pro. Apart from my professional life, I am a big-time foodie and travel enthusiast in my personal life. So, when I am not working, I am probably travelling places to try regional delicacies and sharing my experiences with people through my blog.